Would a 'Medicare for All' plan help you save money on your family's health-care costs? It's complicated - CNBC

The current health-care system is failing too many Americans. A staggering number of people are being forced into bankruptcy over their medical bills, or perhaps worse, avoiding treatment in order to stay afloat financially.

Health-care expenses have become so burdensome that there are a quarter of a million medical campaigns listed on GoFundMe each year, raising about $650 million to help families manage health-care costs.

The nation is reaching a breaking point and as a result, 2020 presidential candidates are starting to weave that hardship narrative — and their proposed solutions — into their policy proposals and stump speeches. Of the 10 Democratic presidential candidates involved in Thursday's debate, six have released detailed proposals for revamping America's health-care system.

But most Americans don't understand how these proposals will work. A June Kaiser Family Foundation poll found that 69% of Americans believed they would still pay deductibles and copays even though the "Medicare for All" plans eliminate those out-of-pocket costs. And over half of those who have workplace health insurance believe they will be able to keep their coverage, even though the Medicare for All plans would set up a new national health-care system and eliminate the need for private insurers.

The current Medicare system is a federal health insurance service for more than 60 million Americans over the age of 65, as well as those with qualifying long-term disabilities who can apply at younger ages.

Sounds simple, right? Wrong. Medicare costs are broken down into a series of plans, known as Parts A through D. Most of those on Medicare don't pay for Part A, which is hospital insurance. But if you do spend time in a hospital, there's a $1,340 deductible. If you're in the hospital for more than two months, you will need to pay $341 per day and beyond 90 days, that jumps to $682 per day, according to Medicare.

Medicare Part B covers medical services, which includes outpatient care, preventive doctor's visits, ambulatory assistance and health-care equipment. Currently, the standard Medicare Part B premiums are usually $135.40 a month or higher, depending on your income.

Parts A and B are referred to as "original Medicare" and virtually all U.S. senior citizens have this coverage. But many also opt for Part C, known as Medicare Advantage, which is supplementary coverage for expenses not included in Parts A and B.

Another big cost for those on Medicare is Part D, the prescription drug coverage. Prices vary by plan, but the average basic premium was about $33 a month this year, although some plans can charge deductibles of over $400.

According to an in-depth Kaiser Family Foundation study published last year, the average Medicare beneficiary paid $5,503 in 2013. Those costs included monthly premiums, as well as services such as long-term care, eyeglasses or contact lenses, hearing aids and dental work, which are not covered by Medicare.

That spending level has increased since 2013, however. Premiums alone have gone up from $105 a month in 2013 to $135 a month in 2019 for the standard Medicare Part B. Medicare estimated that in 2017, participants in good health and on Parts A and B alone paid $7,620.

So if Americans are spending thousands while on Medicaid, then what's the damage for those with traditional employer-based health insurance?

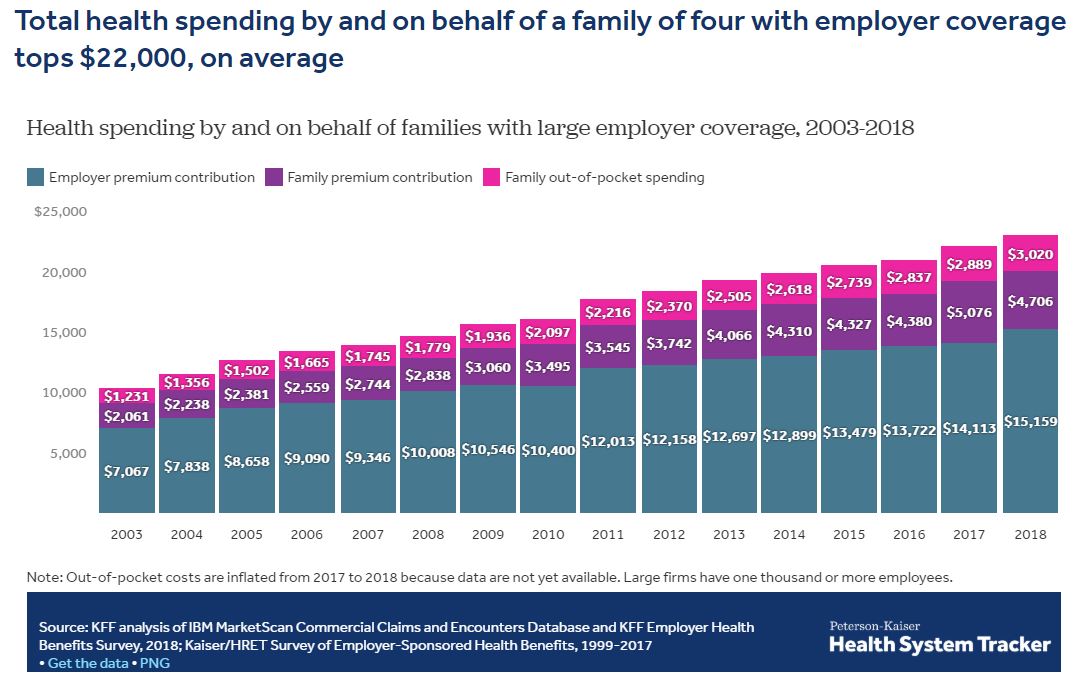

It depends on a variety of factors, including where you live, the size of your employer and your level of health. Looking broadly, the average American family of four with medical insurance spent about $7,726 on health care last year — roughly $4,706 on premiums and $3,020 on out-of-pocket spending, according to KFF.

On an individual level, however, the costs are actually less. An average, healthy American with insurance making $50,000 a year is paying $2,220 in premiums and out-of-pocket costs, according to KFF. Over half of Americans, 59%, say they paid over $500 for out-of-pocket medical costs in 2018, while 5% say they paid over $1,000, according to a survey from TransUnion Healthcare.

Currently, about 92% of Americans have some form of health insurance, with 55% of those with insurance on an employer-based plan, according to the latest U.S. Census Bureau report. Yet the number of Americans with health insurance dropped for the first time last year, due in part to political efforts to weaken the Affordable Care Act passed in 2010.

Yet experts agree that wages are not keeping pace with the rising costs of health care. "There is growing evidence that cost protections have eroded for those who have employer-sponsored health coverage, putting the burden of health-care costs on workers and their families," says David Blumenthal, president of the health-care policy foundation Commonwealth Fund.

And those health-care costs can skyrocket when faced with unexpected or persistent expenses. One in six Americans say they had a surprise medical bill, despite having insurance. The average out-of-pocket cost for an unexpected out-of-network emergency room visit in 2016 was about $628, while those who were admitted paid an average of $2,040, according to a 2019 study published in JAMA Internal Medicine.

Research from the New York Times, the Commonwealth Fund and the Harvard T.H. Chan School of Public Health found that nearly a third of those who are routinely sick, even though they had medical insurance, still spent all of their savings. In fact, a study released earlier this year found that two-thirds of bankruptcies in the U.S. are tied to medical debts.

On the surface, the average person currently spends less on out-of-pocket costs when using a private, employer-based insurance than Medicare. But there are a lot of factors not captured in the data, including the fact that Medicare currently serves a predominantly elderly population who typically require more health care and therefore spend more.

Those who suffer from chronic or severe illnesses are perhaps a better comparison. In the research sponsored by the New York Times, 11% of those who are seriously ill report spending over $50,000 annually on their health insurance and prescriptions. For those individuals, a Medicare for All plan may help them save tens of thousands of dollars each year.

Adding to the challenge of deciding which system would serve Americans better is the fact that Democrats' Medicare for All plans come in a variety of flavors. At its most ambitious, this type of health-care system would replace all the current public and private forms of medical coverage. As a result, the program would not resemble the Medicare system as it stands today.

Beyond the uncertainty around what a dramatic overhaul would mean for Americans' health-care options, critics and even supporters of the Medicare for All proposals also question how the country would pay for such a system. At the very least, such an expensive national program would likely increase many Americans' indirect health-care costs. Currently, the average American making $50,000 with medical insurance already pays an average of $3,050 toward state and federal taxes that fund health-care programs.

https://twitter.com/NBCNews/status/1144054593233592320

"Medicare for All would require a major change in the way in which health coverage and care is organized and financed in the U.S.," Tricia Neuman, director of KFF's program on Medicare policy, said during a testimony in front of Congress earlier this year.

But major changes may be exactly what's needed to solve the financial burdens facing many Americans who need medical help, according to candidates such as Senators Bernie Sanders (I-Vt.) and Elizabeth Warren (D-Mass.). Both candidates have indicated they supported ending private insurance, with Warren taking aim at insurance companies' business model during the June debate.

The goal of these companies, she says, is to "bring in as many dollars as they can in premiums and pay out as few dollars as possible for your health care," Warren said. "That leaves families with rising premiums, rising co-pays, and fighting with insurance companies to try to get the health care that their doctors say that they and their children need."

Don't miss: Americans are staying silent on student loan debt—and it's not helping

Like this story? Subscribe to CNBC Make It on YouTube!

About bd24time.com

No comments